Tips to protect beneficial insects in an IPM program

21 February 2022

Aussie potatoes mashing previous records

21 February 2022

Reading Time: 5 minutes

AUSVEG Advocacy Update – 18 February 2022

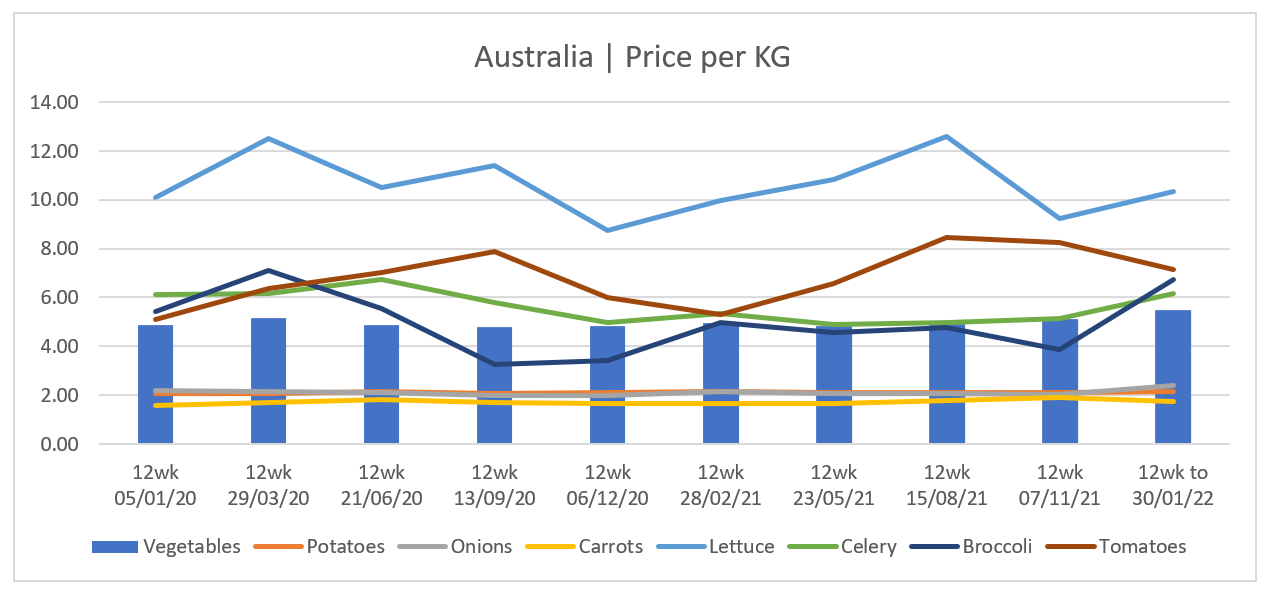

Vegetable and potato prices have remained stable over the last two years despite record rises in farm input costs.

The latest data from Harvest to Home indicates that retail prices for produce have remained at pre-pandemic levels while growers face increases of more than 40 per cent in fertiliser, chemical and fuel costs, and increases by more than 20 per cent in wages and even airfares.

For growers to receive a fair price for their produce, vegetable and potato prices must increase.

AUSVEG is calling on retailers and buyers to ensure that farmgate prices that growers receive for their produce better reflect the current economic climate to ensure the financial viability of vegetable and potato producers.

AUSVEG calculation based in part on data reported by NielsenIQ through its Homescan Service for the Vegetables category for Total Australia, according to a client defined product hierarchy. Copyright © 2022, Nielsen Consumer LLC.

The table below demonstrates that, while there is some seasonal variation in prices of some vegetable commodities over the last two years, the percentage change in retail price is not matching input cost increases. This shows that growers are taking the hit.

| Commodity | January 20 price ($/kg) | Current price ($/kg) | Percentage change |

| Revenue | |||

| Potatoes | AUD$2.07 | AUD$2.16 | 4.34% |

| Onions | AUD$2.19 | AUD$2.41 | 10% |

| Carrots | AUD$1.59 | AUD$1.73 | 8.8% |

| Lettuce | AUD$10.08 | AUD$10.35 | 2.67% |

| Celery | AUD$6.13 | AUD$6.15 | 0.3% |

| Broccoli | AUD$5.44 | AUD$6.75 | 24% |

| Average | AUD$4.58 | AUD$4.92 | 7.5% |

| Cost | |||

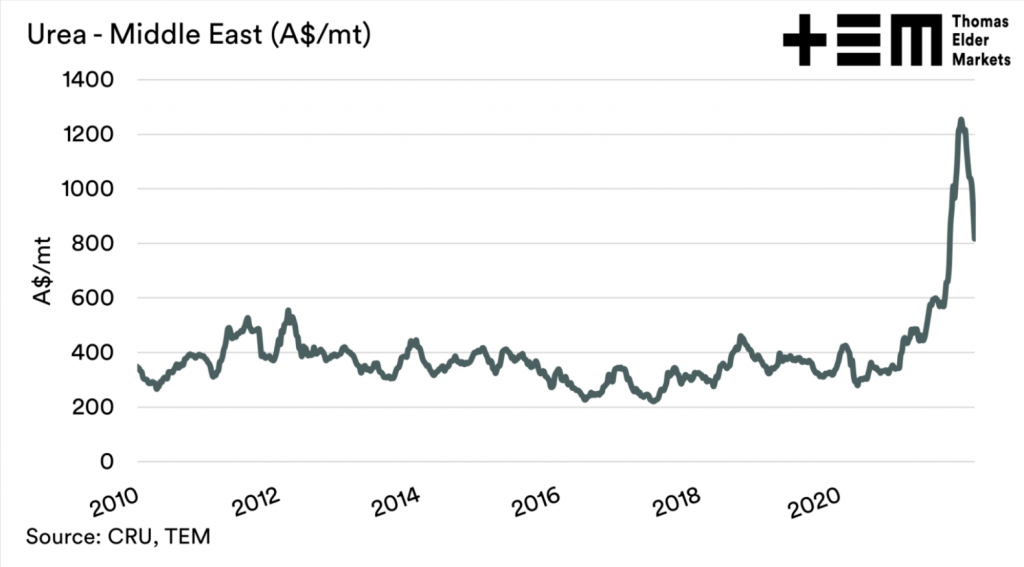

| Urea | AUD$300/mt | AUD$815/mt | 171.7% |

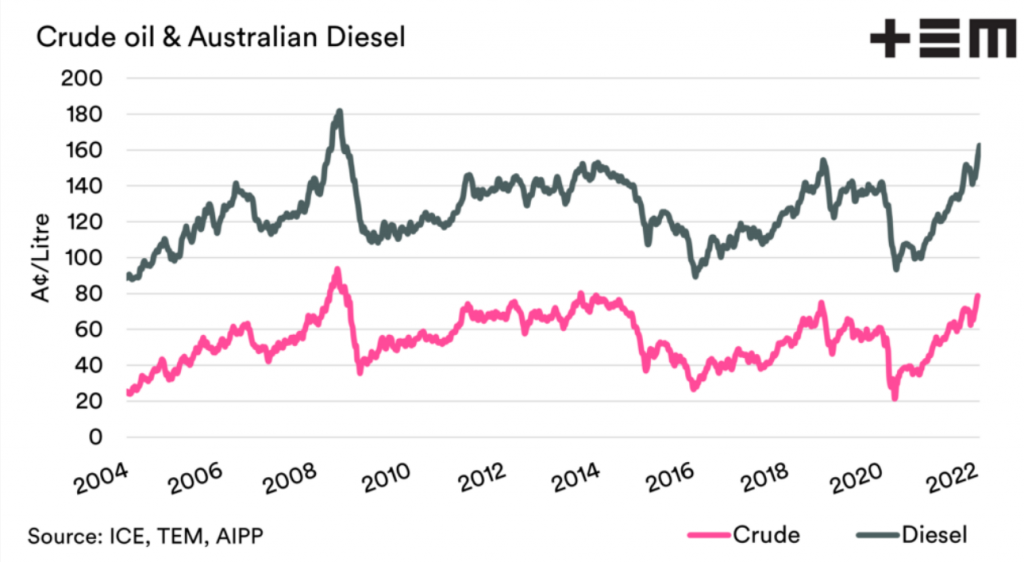

| Diesel | AUD$1.35/lt | AUD$1.65/lt | 22.2% |

| DAP/MAP | AUD$312.4/mt | AUD$699.4/mt | 123.9% |

| Fertilisers | AUD$73.2/mt | AUD$200.6/mt | 174% |

| Crude Oil | USD$57.34/bbl | USD$91.590/bbl | 59.7% |

| Average | 110.3% |

The below table also highlights the significant disparity between the change in vegetable prices over the last two years when compared with other agricultural commodities that are also facing cost increases.

| Commodity | Jan 2020 | Current price | Percentage change |

| Vegetables | AUD$4.58/kg | AUD$4.92/kg | 7.5% |

| Wheat (APW) | USD$569/bu | USD$795.50/bu | 39.80% |

| Canola | CAD$478.3/t | CAD$1011.30/t | 111.4% |

| Cattle (EYCI) | 477c/kg cwt | 1,127c/kg cwt | 136.3% |

| Trade Lamb | 702c/kg cwt | 828c/kg cwt | 17.9% |

| Milk | USD$17/cwt | USD$20.88/ cwt | 22.8% |

| Cotton | USD$70.3/lbs | USD$121.93/lbs | 73.4% |

| Average | 58.4% |

It is important to note, that while each agricultural commodity is different and the scale of which farmers use fertiliser, chemicals, fuel, labour etc varies, they still all use these farm inputs, and they have all risen substantially.

The comparative data represents a vastly different trend between the commodities.

Vegetable prices have seen the lowest percentage increase in price across all the agricultural commodities, at an average of just 7.5 per cent across the subset of vegetable crops highlighted above.

This is well below the average percentage of agriculture commodities of about 59.2 per cent, and also well below the average percentage increase of the input costs at a massive 110.3 per cent.

These are alarming numbers and go to the heart of the supply chain issues within the fresh produce industry.

Many growers have contacted AUSVEG highlighting their frustration and the challenges their businesses are facing to remain viable during this difficult time.

The current price challenges cannot continue – growers deserve a fair price – and AUSVEG will continue to highlight these issues to government and other relevant stakeholders.

Below is a snapshot of some key farm input costs and commentary from Thomas Elder Markets.

Overview

Towards the end of 2021, the price of fertiliser was starting to drop slightly, which was a result of the falling price of gas and oil. However, there are reports that Australian fertilizer suppliers were not passing these reduced prices to farmers this financial year as they are still trying to offload inventory purchased at a higher price.

As a result, growers have begun to delay purchasing and rationing their fertiliser supply, which could lead to production shortages and higher food prices. Some growers have also begun looking into alternatives such as Nitrogen fixing pulses and manure; however, the supply of these is heavily dependent on location and availability.

The effects of China closing its doors on exports has left a gaping hole in supply of fertilisers around the world. Russia, which was supplying some of Australia’s Ammonium Nitrate fertilizer, is also now concerned for the supply for their domestic farmers and has banned exports as a precaution.

Luckily Russia is not a major supplier in the Australian market, so this should not have as big an impact on Australia’s supply as the decision from China.

Ag Chemical Industry News:

The Ag chemical industry is facing problems with the cost and unreliability of shipments. Many essential ingredients for crop protection products are not being produced or shipped by key countries.

Strike Energy’s Project Haber has been awarded Major Project Status by the Federal Government. The project has the potential to offer major downstream opportunities and significantly reduce Australian farms’ carbon output. The plant could supply Australia with 96 per cent of local urea needs. The Federal Government has contributed $225 million towards the $4.3 billion plant. The plant will produce two million tonnes of granular urea fertiliser per year and will help to create a secure supply for Australian growers.

Some key facts about the supply farm inputs:

Urea

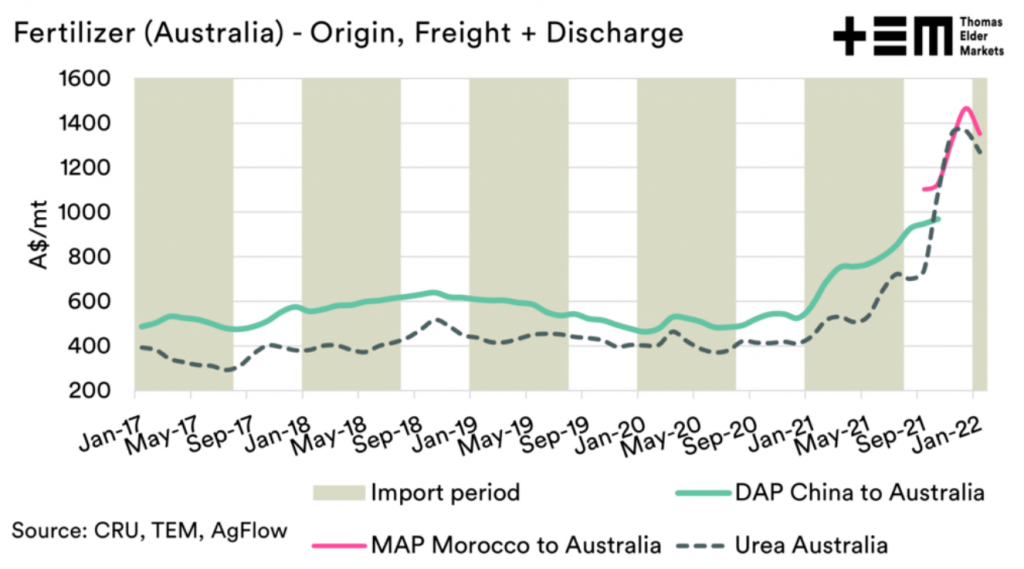

- The price of imported urea was 74 per cent higher in September 2021 than the average for 2020.

- Prices have fallen due to increased supply of gas prices in some regions.

- International urea prices have fallen from AUD$1,215 per tonne to $815 per tonne, whilst this is a significant drop it remains far higher than the normal $400-500 per tonne.

DAP/MAP

- Fertiliser prices are still high due to the export ban in China. China is the world’s single largest exporter and supplier, so prices of MAP/DAP won’t change until they begin to export again.

- MAP price was 102 per cent higher in September 2021 than the average for 2020.

Freight

- Freight is likely to remain elevated for 2022.

- Shipping container rates from Australia to Oceania have increased 56 per cent since mid-2020.

- Domestic road freight pricing has increased over the past two years by up to 20 per cent for moving products from farm to market.

Fuel

- Crude oil price is at a seven year high.

- Diesel costs at harvest time, which is the highest use time of year, up 30 per cent for some growers.

- Diesel prices the highest they have been since 2008, due to increase in crude oil prices.

AdBlue

- Incitec Pivot has ramped up its production of AdBlue to keep up with Australian demand. However, the production is looking to cease at the end of this year. Incitec Pivot was producing 450,000 litres per week and is now turning over three million litres per week, which represents a significant increase that has filled 75 per cent of Australia’s demand.

- Incitec Pivot is planning to close this factory at the end of the year regardless of any government grants.

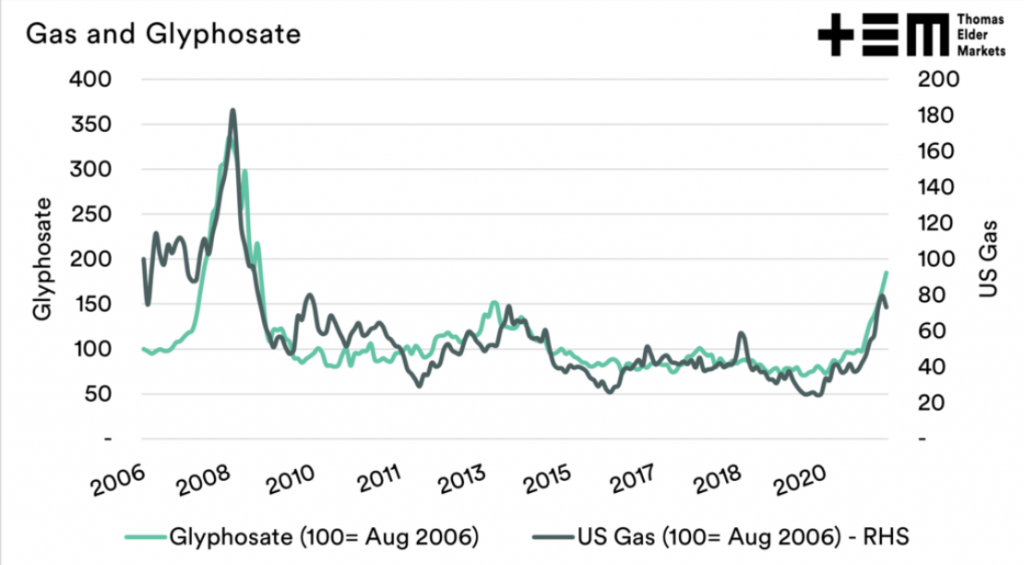

See below for additional data on urea, fertiliser, fuel, and gas and glyphosate.

Read more about the input shortages in the media here:

- High input costs and supply chain challenges stack up | Farm Weekly | Western Australia

- AdBlue: Angus Taylor says no more federal grants (afr.com)

- Fertiliser price fall fails to be passed on to Vic croppers | Stock & Land | Victoria (stockandland.com.au)

- Victorian farmers juggle fertiliser volatility | Stock & Land | Victoria (stockandland.com.au)

- Green light for granular urea fertiliser | Farm Weekly | Western Australia