Safeguarding Australian veg from seedy biosecurity risks

25 November 2021

Natasha Shields: Investigating alternatives to plastic packaging on fresh produce

25 November 2021

Hort Innovation has worked with global information and measurement company, NielsenIQ, to bring growers the largest series of insights into market performance and shopping behaviour yet. As we begin to re-open post lockdown, NielsenIQ has looked at how the produce market has shifted and what behaviours will be key. NielsenIQ Director Llew Stevens reports.

The COVID-19 pandemic has been impacting the way consumers shop and buy fresh produce for almost two years.

As we moved through 2021, we began cycling the extreme purchasing of the first Australian lockdown. Currently, we see total fast-moving consumer goods (FMCG) continue to grow despite experiencing a slow-down as we cycled these high growth periods of 2020 – currently up only 1.6 per cent versus last year, but a strong 13.1 per cent increase versus 2019.

As we start moving into 2022, we will also begin to see the longer-term shifts in customer behaviour and how we may still feel the impacts even after we begin to move past lockdowns. Frequency of trips, after experiencing a sizeable increase during the early days of the pandemic, has contracted back down to below pre-pandemic levels. Meanwhile basket size continued to increase, rising more than AU$5 over the past two years, to sit at an average of almost $49 per trip.

Interestingly, while Victoria contracted in the number of trips per household throughout the past 18 months, consumers were still making more trips the average Australian household despite lockdowns.

Produce trends in 2021

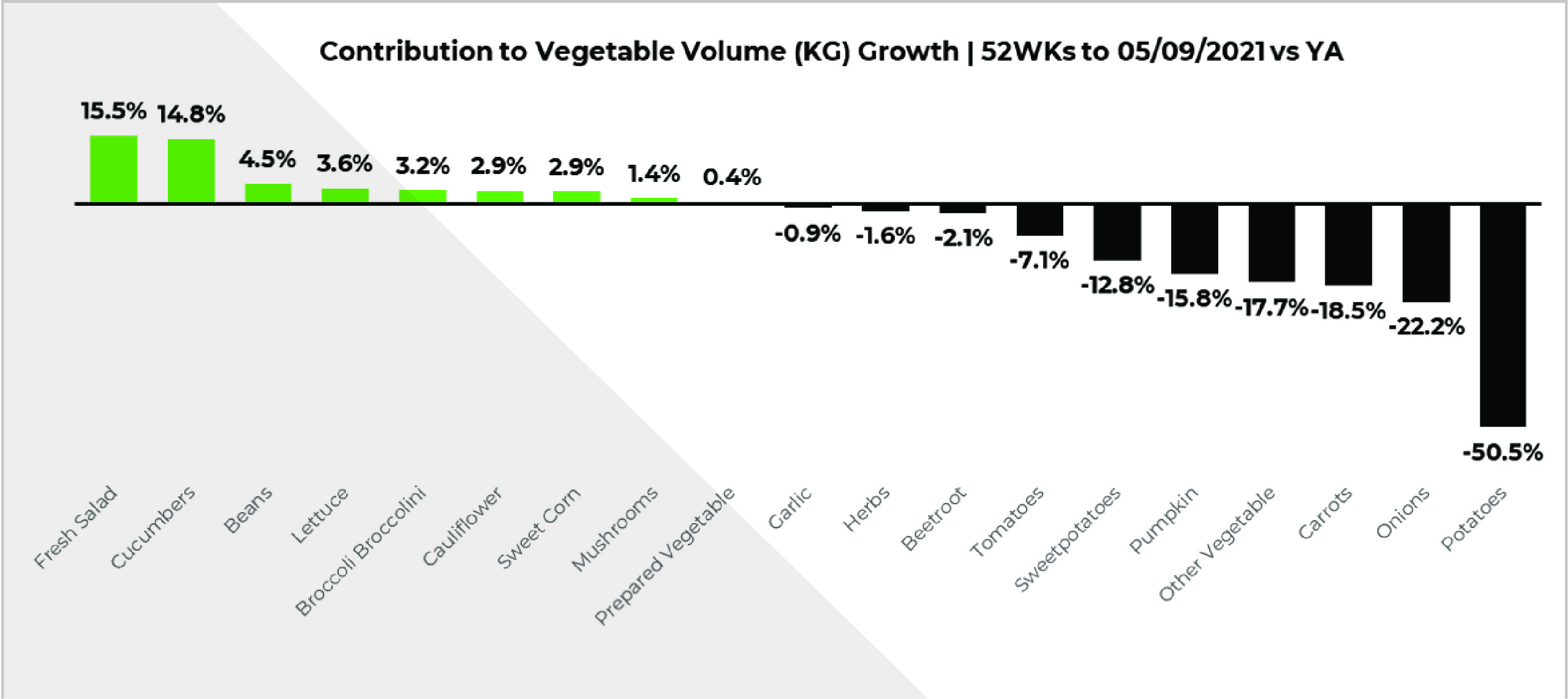

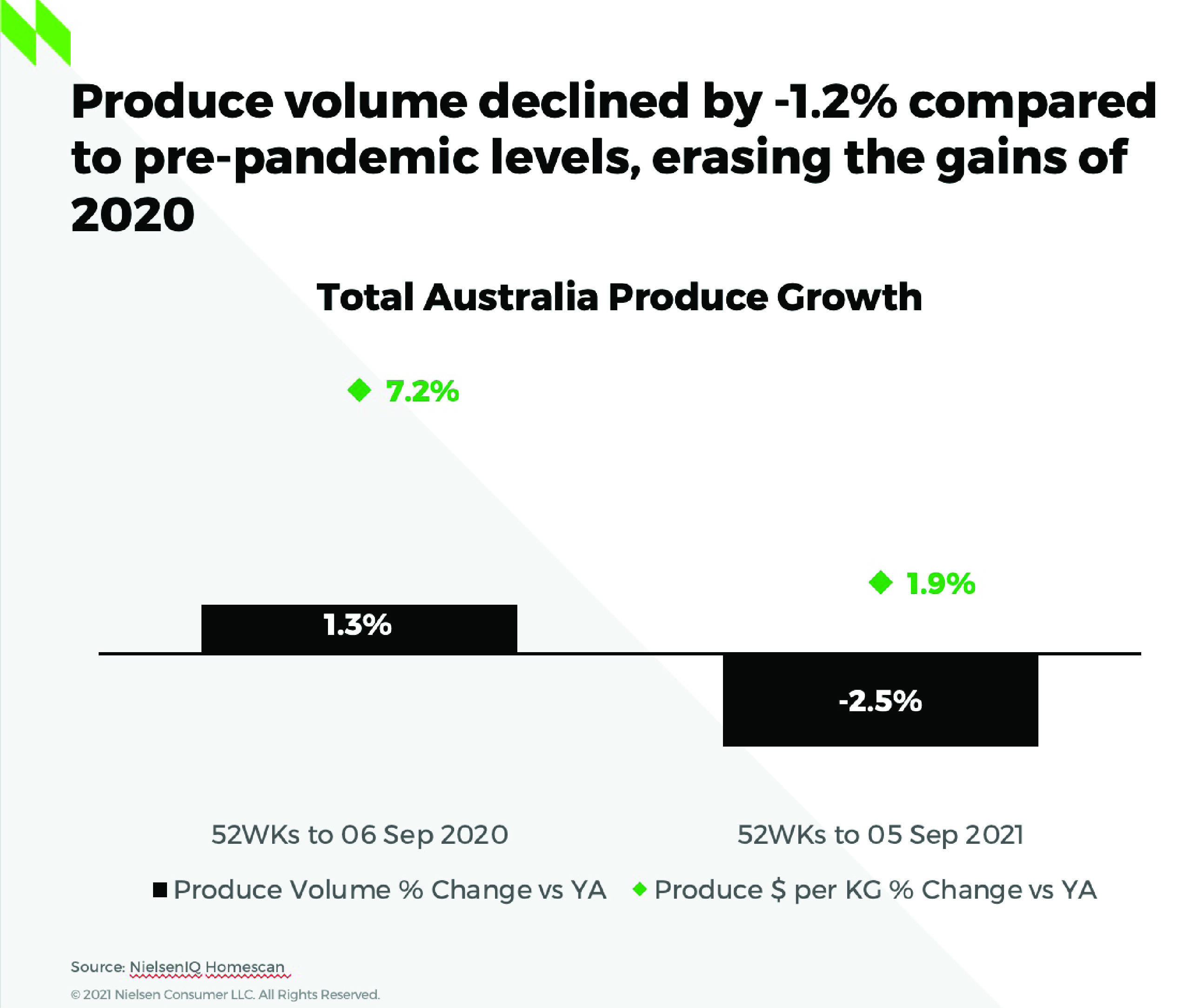

Produce by kilogram (kg) volume declined by 1.2 per cent compared to pre-pandemic levels – erasing the gains of 2020 – with both fruit and vegetables in volume decline versus 2020. This decline was seen across almost all of Australia with all mainland states declining in kg volume versus 2020, and all except Victoria seeing volume kg decline versus 2019 – however the NT was an exception, with growth versus 2019 and 2020.

Potatoes stood out in the vegetable category as the largest driver of declines versus last year, where it was the biggest driver of gains in NielsenIQ’s summer 2020 update. This turnaround was driven primarily by the strength of potatoes during those early pandemic months of March to May 2020 where we saw around 63 per cent of Australian households purchasing potatoes in each of those months, with strong volume gains to show for it.

In 2021, we saw household penetration hover between 55 per cent to 58 per cent during those months – more in line with its long-term monthly average – as well as reduction in average trips and volume of potato purchased per trip. So, while there were sizeable declines at the yearly level these came predominantly from cycling through the high growth we saw in early 2020.

This year also saw a consolidation of spend back into major supermarkets (Woolworths, Coles, and Aldi) as the increased repertoire of 2020 faded. Currently they sit on a combined 75.5 per cent share of produce value – up from 74.3 per cent last year, and higher than their pre-pandemic share of 75 per cent in 2019 – leaving major supermarkets well-positioned as we head into Christmas 2021.

2022 trend predictions

There will be greater consolidation into major supermarkets – online and bricks and mortar – as customers are already doing fewer trips as they seek to make the most of it. Throughout the pandemic, we’ve seen online grocery shopping jump from 3.5 per cent of produce dollar sales up to 7.3 per cent in the latest year. While growth may slow as we exit lockdown and more normal shopping behaviours have a chance to resume, it can be hard to break a habit you’ve spent 18 months building.

Shelf stability and long-term freshness will be key for producers as households will make fewer fresh top-up shops. Fewer trips to the shops mean fewer chances to pick up fresh produce, as well as longer lags between trips. Longer shelf stability will help ensure customers have the best chance for getting fresh produce when they shop, and that it stays fresh once they get it home.

Prices for produce will be top of mind as the impacts of supply booms and shortages continue to work their way through the supply chain both globally and locally. As some prices continue to increase due to constraints – while others reduce thanks to seasons of high supply – customers will need to be savvy to get the most out of their grocery spend.

Sources: NielsenIQ Homescan Data to 05 September versus Prior Year and versus Two Years Ago.

Find out more

Please contact Llew Stevens at Llew.x.Stevens@NielsenIQ.com.

These data and insights were produced independently by NielsenIQ and shared through the Harvest to Home platform, supported through the Hort Innovation vegetable, sweetpotato and onion research and development levies. For more insights, visit harvesttohome.net.au.

The Harvest to Home dashboard is an initiative of the Vegetable Cluster Consumer Insights Program and is funded by Hort Innovation using the vegetable, sweetpotato and onion research and development levies and contributions from the Australian Government.

Project Number: MT17017